Interrupted supply chain and decreased sea freight output have been deeply footprinted by the global 2-year pandemic expansion, resulting in the record increase in freight. Continuously hitting the new top freight makes the export sector “shoulder” an ocean of hardship without a clear end time. How is the rate “cooled down” to help the export businesses to obtain more chances?

More serious impact on routes from Asia is found against that in the reverse extreme. For instance, Shanghai – Rotterdam (Netherlands) route and Shanghai – Los Angeles (the USA) route are found with a 6-time increase while

Rotterdam – Shanghai and Los Angeles – Shanghai way is only increased by 34% and 99%, respectively, against the same

period.

Vietnam export categories have been seriously hit by the increased freight, including the most affected exports from Vietnam to the EU and North America.

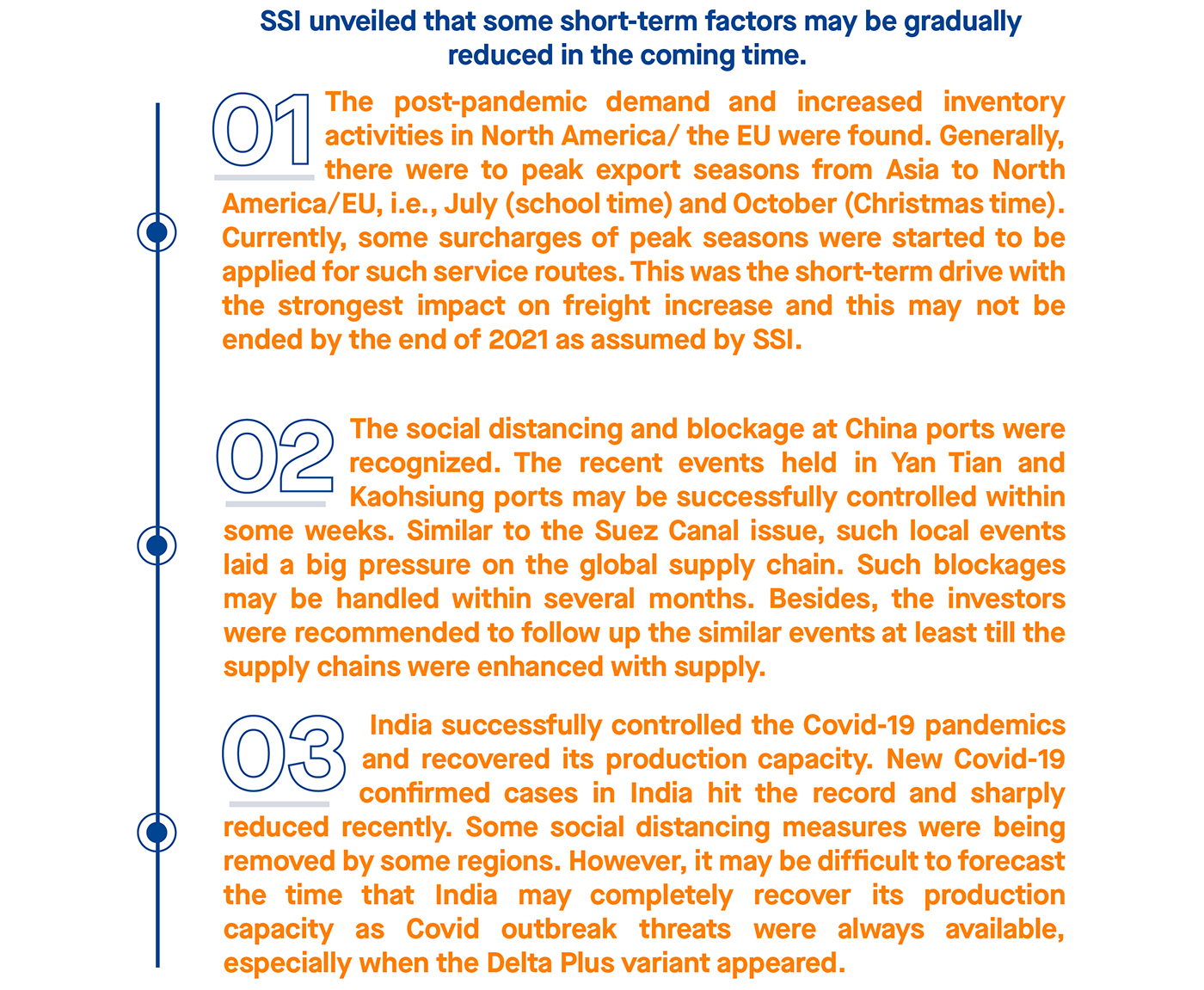

By analyzing the increased sea freight causes, SSI specified that The root cause was originated from prolonging Covid-19 pandemics. The sea transportation service providers started to reduce costs by suspension, trip cancellation, and

de-acceleration of vessels to reduce the fuel costs. This reduced the large-scale capacity for a series of global main transportation routes. Total container fleet capacity reduced by 18% in May 2020 as referred by Drewry

Moreover, the ports’ handling capacity was also reduced due to worker unavailability and long quarantine time, resulting in serious blockage at ports and delays in container handling. Furthermore, the social distancing and traveling restrictions were applied in many countries in the world, especially the USA and the EU, resulting in the fact that their local production capacity was remarkably reduced.

The very high rental of containers was pushed up by container inadequacy and some exporters also struggled with difficulties in looking for an empty container for packing.

In the long run, some factors may lead to the existence and maintenance of freight at a higher level than the pre-Covid-19 average one, including Strengthening

cooperation in controlling the supply and price among carriers due to the establishment of

affiliation and more M&A in the recent years. For example, CSCL and OOCL were merged as COSCO Group, APL was merged with CMA CGM, UASC was merged with

Hapag-Lloyd, and ONE affiliate was established, including K-Line, MOL, and NYK.

Such moves enhanced the vessel carrier’s strength, making the freight hard to restore to its low level as what had happened from 2008 to 2019. In the context of increased oil price, the carriers are forecast to de-accelerate as much as possible to save fuels, resulting in slower container circulation and higher freight.

From the aforesaid analysis, the freight is forecast to hit the top in Q4/2021 and lightly adjusted in the first half of 2022. The freight may be remarkably reduced by 2023 when the new vessel supply is put into operation. However, the higher rate than it of the pre-Covid pandemic is still maintained. Drewry unveiled that the

average charge may increase by 23% this year and it may lightly reduce to 9% in 2022 as the demand restores to the normal level. Meanwhile, the long-term freight may be still higher than that before COVID-19 outbreaks.

In response to the prolonged difficulties, the recommendations on addressing the container inadequacy and restore the vessel freight rate to the rate in November 2020 have been recently submitted to the MARD and the Prime Minister for

consideration and approval by Vietnam category associations and VASEP for

example.

In addition to the analysis on super-increased freight and overlapping difficulties struggled by the businesses, VASEP also reported the situation that the higher rate is accepted to receive a higher booking. If the agent-based booking was easier than the direct booking at vessel carriers, the question is that container and space were “pinned” by the carriers to push up the container rental. This was illogical in the context that the oil price (the highest cost of the carriers’ operating costs) is much lower than that previously. The carriers also had a long time from Q4/2020 to

supplement the number of insufficient vessels and containers.

That is why VASEP recommended that if no controls are taken by the concerned agencies and industries, this situation shall be prolonged with increasingly high sea freight and inadequacy of containers, adversely affecting the seafood export in

particular and Vietnam export categories in general.

If the above issues are successfully addressed, the freight shall be “cooled down” and the exporters shall be given more opportunities to further develop. During

controls of sea vessel rates are pended for, alternative transportation solutions may be used such as railway transportation. On 20 July, container fleet transporting

garment and textile and leather shoes were directly accessed to Belgium from

Vietnam, opening a new transportation route to the EU, as initiated by Ratraco in combination with the cross-border carriers and forwarders involving in logistic

service supply for Vietnam to the EU customers. Currently, Ratraco and the EU

partners have started to plan and develop the 8 trips per month from Vietnam to transport items including electronics, garments, textile, leather shoes, cosmetics, frozen foods and foodstuff, fruits, etc.

With a series of outstanding advantages such as low cost, correct schedule, great bulk transportation, long-distance, outstanding safety, and railway transportation service may be recognized as an optimal transportation solution alternative for

businesses, especially in this hard time.

Comment